You know that feeling when your car starts making a weird rattling noise, and your stomach instantly drops? Or when you look at the calendar, realize Christmas is two months away, and you have exactly zero dollars saved for it?

The first time my car broke down, and I had zero savings for it, I put the repair on a credit card and cried about it for a week. I felt like a complete failure.

If you have ever been blindsided by a bill and thought, “I should have seen this coming,” you are not alone. And more importantly, there is a simple fix.

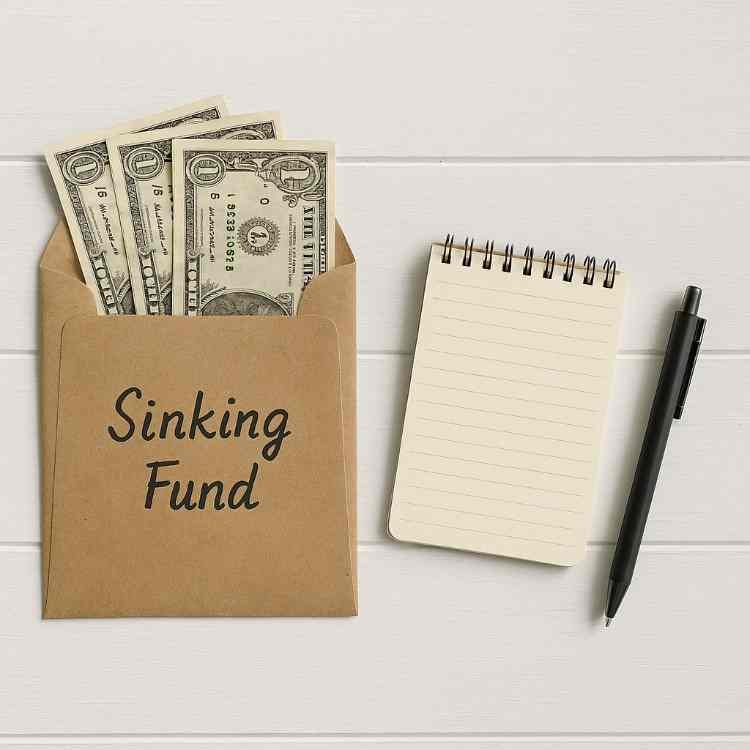

It is called a sinking fund.

Here is the thing… a sinking fund is the ultimate stress-reliever for your budget. It turns giant, terrifying expenses into tiny, manageable monthly bites.

By the end of this post, you will know exactly what a sinking fund is, why you need one even on a tight budget, and how to start yours today — with whatever money you have right now.

What Is a Sinking Fund?

A sinking fund is a strategic way to save money by setting aside a small amount each month for a specific, known future expense. Instead of pulling from your regular checking account when a big bill arrives, you build up a dedicated cash reserve over time.

According to NerdWallet, this method keeps you from blowing your budget on planned expenses.

Think of it like this. If you know your car registration is $120 a year, you do not wait until the bill comes to panic. You save $10 a month. By the time the bill arrives, the money is just sitting there waiting.

It really is that simple.

Another example is a Christmas fund. If you want $240 for the holidays, you save $20 a month all year long. Come December, you pay for gifts with zero debt.

Dave Ramsey recommends using this method to stop relying on credit cards for things you know are going to happen.

Let me be real with you. The first time I used a sinking fund for my car insurance, the bill arrived, and I actually smiled. I handed over the money and felt relief instead of absolute panic. It changed everything for me.

Even $10 saved on purpose beats $0 saved by accident.

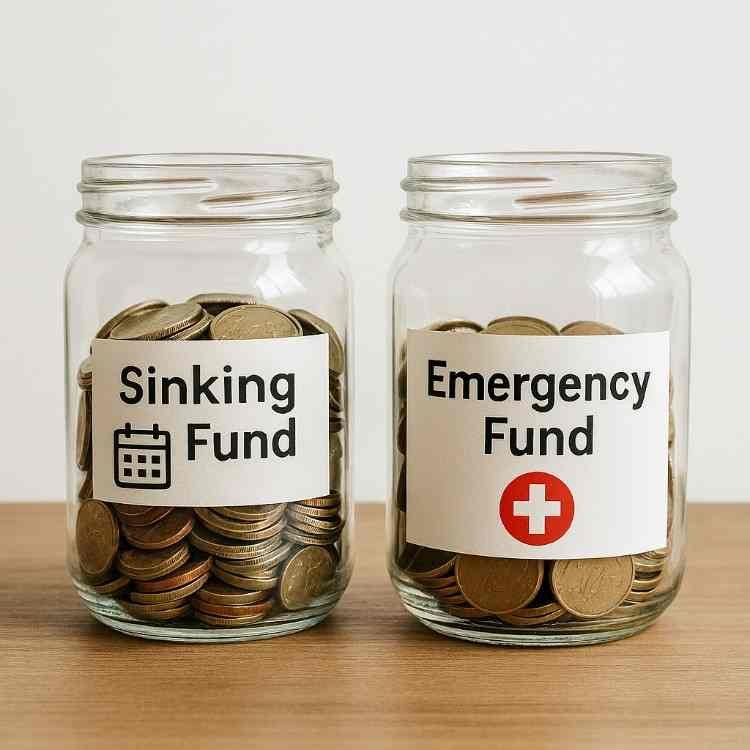

Sinking Fund vs Emergency Fund: What Is the Difference?

A sinking fund is for planned future expenses, while an emergency fund is for completely unexpected financial crises.

You know those surprise bills that pop up? Some are true emergencies, but most are just poor planning on our part. If you are living on a bare-bones budget, you absolutely need both. They do entirely different jobs for your money.

Here is exactly how they compare:

| Sinking Fund | Emergency Fund | |

| Purpose | Planned future expenses | Unexpected emergencies |

| Examples | Car repair, holidays, back to school | Job loss, medical crisis, accident |

| Amount | Spend it when the goal arrives | 3-6 months expenses |

| How to use | Only touch in a true emergency | Only touch in true emergency |

| Mindset | Expected expense | Unexpected crisis |

An emergency fund protects you from life’s major storms. A sinking fund pays for the rain jacket you knew you would need.

Think of your emergency fund as your fire extinguisher. Your sinking fund is your maintenance schedule that stops fires before they start.

Why Low-Income People Need Sinking Funds More Than Anyone

When you are living paycheck to paycheck, the idea of saving money feels like a cruel joke. I get it. Money is already incredibly tight.

I remember making just enough to cover my rent and groceries. One month, an unexpected $200 dental bill completely destroyed my whole month. We ate buttered noodles for two straight weeks just to survive.

But here is exactly why you need a sinking fund on a low income.

1. You cannot afford surprises

When every dollar is already spoken for, one unexpected bill does not just hurt — it wipes you out. A sinking fund acts as a shock absorber.

2. It breaks the debt cycle

Without a plan for expected expenses, credit cards and payday loans become the only option. And figuring out how to get out of debt is much harder once you are trapped in that cycle.

3. It builds real confidence

There is something powerful about knowing the car registration is covered before the bill arrives. You stop feeling like a helpless victim to your bills.

4. It works even with $10/month

You do not need a high income. You need a small, consistent habit. Trust me — when you sit down and really look at your spending, that $10 is hiding somewhere.

Trust me on this one. You can do this.

How to Start a Sinking Fund on a Low Income: Step by Step

I know this sounds almost too easy, but the simplest systems are the ones that actually work.

Here is exactly how to start a sinking fund for beginners, even if you feel totally broke right now.

1: List Your Upcoming Planned Expenses

Think about the next 12 months. What is coming that costs money? Write it all down.

Get a piece of paper and think about your car registration, back-to-school supplies, Christmas, annual subscriptions, or medical copays. Get it all out of your head.

2: Pick Your Most Urgent 1 or 2 Goals

Do not try to save for 10 things at once. Pick the most urgent and start there.

If your tires are balding, start a car maintenance fund immediately. If December is creeping up, start a holiday fund.

3: Do the Simple Math

Now, figure out how much you need to save each month.

Total amount needed ÷ months until needed = monthly savings goal.

For example: $300 car repair ÷ 6 months = $50/month.

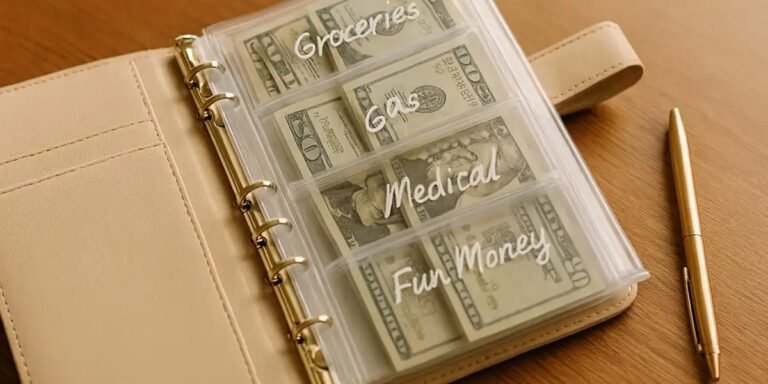

4: Open a Separate Savings Spot

This money needs its own safe spot — completely separate from your spending cash.

You can use a separate savings account at your bank. You can use a labeled envelope using the cash stuffing envelope method. Even a literal jar on your shelf does the job.

5: Save on Payday — Before Anything Else

Move money to your sinking fund the SAME day you get paid. Before groceries. Before everything.

Even $5 on payday is a sinking fund. Do not let a small amount stop you from starting.

6: Do Not Touch It Until It’s Time

This is the hard part. Treat it as if it does not exist until the expense arrives.

No “borrowing” from it for a pizza night. Protect your savings.

7: Celebrate When You Use It

The whole point is to use it. When you pay for that car repair with cash you saved, that feeling is unlike anything else.

The first time I paid for four brand new tires with money from my car maintenance envelope, I walked out of that shop feeling like a millionaire. Zero stress, zero debt.

If you do cash stuffing, add one envelope labeled with your sinking fund goal. Done.

Every small step forward is a victory. You have got this.

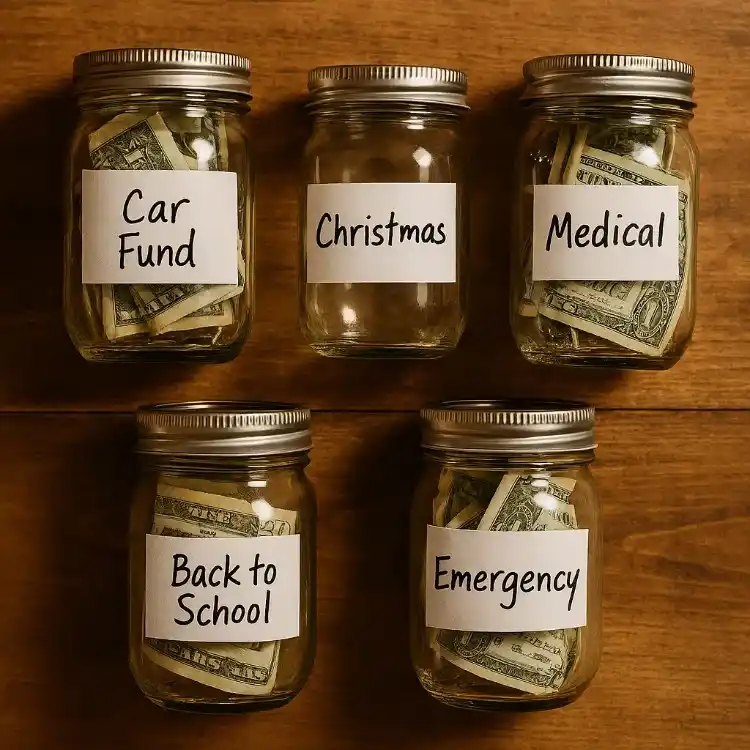

Best Sinking Fund Categories for Low Income

Here is the fun part — figuring out what to save for. These are the categories that matter most when money is tight.

── Start With These 4 Urgent Funds ──

These are the most common surprise expenses for low-income earners.

1. Car Repair / Maintenance

Why: A broken car is the number one budget killer for low-income families. Without a car, you cannot get to work.

How much: $30 to $50/month.

Even older cars need oil changes. Budget it.

2. Medical Copays and Prescriptions

Why: Health emergencies do not wait. Getting sick is expensive, and skipping meds because you are broke is dangerous.

How much: $20 to $40/month.

Dental visits count here, too.

3. Back to School / Kids Expenses

Why: Every August, this blindsides parents. Backpacks, shoes, and school fees add up incredibly fast.

How much: $15 to $30/month saved all year.

Start in January. By August, you have $105 to $210 ready.

4. Annual Bills and Subscriptions

Why: Car registration, renters insurance, Amazon Prime — they come once a year.

How much: Add up your annual bills ÷ 12.

Example: $120 car registration ÷ 12 = $10/month.

── Add These Later When You Have Breathing Room ──

Once your first few savings categories are running smoothly, add these.

5. Holidays and Christmas

How much: $20 to $50/month.

Start in January. Seriously. January. Cut out the things I quit buying to save money to free up this cash.

6. Clothing and Shoes

How much: $10 to $20/month.

Kids grow. Shoes wear out. Budget for it so you never feel guilty buying a winter coat.

7. Home Repairs / Renter Needs

How much: $15 to $25/month.

Even renters need toilet plungers, light bulbs, and the occasional broken item fixed.

8. Pet Expenses

How much: $20 to $30/month.

Vet bills do not care about your budget. Keep your furry friends safe.

── The “Someday” Funds (Your Future Goals) ──

Add these when Group A and B are running perfectly.

9. Vacation or Family Trip

How much: Whatever you can — even $5/month.

You deserve rest. Even a $200 road trip counts as a vacation.

10. Car Replacement Fund

How much: $20 to $40/month.

If your car is old, saving $20/month is smarter than panicking later.

11. Emergency Deductible Fund

How much: Check your policy.

If you have insurance, save for the deductible. Because you will need it when things go wrong.

Here is a quick summary breakdown:

| Sinking Fund Category | Suggested Monthly Amount | Priority |

| Car Repair | $30 to $50 | 🔴 Start Now |

| Medical/Copays | $20 to $40 | 🔴 Start Now |

| Back to School | $15 to $30 | 🔴 Start Now |

| Annual Bills | Your bills ÷ 12 | 🔴 Start Now |

| Holidays/Christmas | $20 to $50 | 🟡 Add Next |

| Clothing | $10 to $20 | 🟡 Add Next |

| Home/Renter Needs | $15 to $25 | 🟡 Add Next |

| Pet Expenses | $20 to $30 | 🟡 Add Next |

| Vacation | $5 to $20 | 🟢 Dream Fund |

| Car Replacement | $20 to $40 | 🟢 Dream Fund |

Start with 1 or 2 from Group A. Master those. Then add more.

Small and consistent beats big and abandoned.

Real Example: Sinking Fund Plan For $1,000/Month Income

It is easy to talk about saving money, but let us look at real numbers.

If you are following the 50/30/20 rule for low income, finding extra cash is tough. But look at this realistic, bare-bones sinking fund plan.

| Sinking Fund | Monthly Amount |

| Car Repair | $30 |

| Medical Copays | $20 |

| Back to School | $15 |

| Car Registration | $10 |

| Holidays | $20 |

| Clothing | $10 |

| TOTAL | $105/month |

Yes, $105 sounds like a lot when money is tight. But break it down — that is $26 a week. Less than one takeout meal.

If you use a solid, bare bones budget template, you can find that $26.

Even if you can only do $30/month total right now, start there. Pick 1 category.

You have got this.

Common Sinking Fund Mistakes Beginners Make

We all mess up when we first start budgeting. And that is okay.

Avoid these traps, and you will be fine.

1: Trying to Start 10 Sinking Funds at Once

Pick 1. Just 1. Start there. If you try to save for a dozen things, you will get overwhelmed and quit.

2: Keeping It in Your Regular Account

If it is mixed with your spending money, you will spend it. Separate it immediately.

3: Saving Irregular Amounts

Some months $50, some months $0 — this does not work. Even $10 consistently beats $100 randomly.

4: Using It for Non-Emergencies

Your sinking fund has a job. Do not reassign it without a good reason. Tapping your car repair fund for a pizza delivery is one of those toxic money habits we have to break.

5: Giving Up After a Bad Month

Missed a month? Add it to next month. That is it. No drama.

Perfection is not the goal. Progress is.

5 Quick Tips to Make Your Sinking Fund Actually Work

Ready to crush your goals? Here are my favorite tips.

- 1: Name your sinking fund after its goal

Not ‘Savings’ — label it ‘Christmas 2026’ or ‘Car Fund.’ Named money is harder to spend.

- 2: Automate it if possible

Set up an auto transfer on payday. What you do not see, you do not spend.

- 3: Use cash envelopes if you are visual

Physical cash in a labeled envelope makes it real. The cash stuffing method is perfect for this.

- 4: Track your progress visually

Draw a simple savings thermometer on paper. Color it in each month. Old school works.

- 5: Celebrate every $50 milestone

Progress feels good. Let yourself feel it.

Making Saving Simple Again

If money has always felt like one emergency away from disaster — that is not your fault. That is a system that never taught us this stuff.

Walking into a mechanic shop or a dentist’s office with the cash already sitting ready changes your entire relationship with money.

No, seriously. We are all just doing the best we can.

A sinking fund does not require a high income. It requires a small, consistent decision. Whether you save $5 a week or $50, you are building a safety net that will change how you feel about your finances. You are taking control.

You are doing so much better than you think, and I am proud of you for starting.

Now I want to hear from you. What is the first sinking fund category you are going to start? Drop it in the comments — I read every single one.

Still have questions? I had all of these when I started. Here are the ones I hear most:

Frequently Asked Questions

A sinking fund is money you set aside in small amounts every month to pay for a specific, known expense in the future. Instead of going into debt when a big bill arrives, you use the cash you have slowly saved up. It makes large expenses affordable by breaking them down into simple monthly pieces.

You can start a sinking fund with as little as $5 a paycheck. You do not need to be rich or have hundreds of dollars leftover at the end of the month. Starting small is exactly how you build the habit, and those tiny amounts add up incredibly fast over time.

You should keep it completely separate from your daily checking account. You can open a separate high-yield savings account, use a labeled cash envelope, or even drop money in a physical jar. The most important thing is that you cannot easily swipe your debit card and spend it on impulse.

No, they are completely different. A sinking fund is for planned, expected expenses like Christmas gifts or annual car registration. An emergency fund is for massive, totally unpredictable crises like a sudden job loss or a major medical emergency.

A beginner should stick to 1 or 2 at most at first. Focus on your most stressful upcoming expenses, like car repairs or an upcoming holiday. Once you master the habit with one or two, you can slowly add more categories without feeling overwhelmed.

Yes, and you are exactly the person who needs it most. When your budget is incredibly tight, even a tiny $50 unexpected bill can cause massive panic. Saving just $5 or $10 a month protects your paycheck from being wiped out by surprise expenses.