I was sitting in my car outside the grocery store. My stomach was in knots. I opened my banking app, hoping the electric bill had not cleared yet. It had. I had fourteen dollars left to feed myself for six days. I know how that deep, heavy shame feels. You work hard, and you should not feel this broke. You are not bad with money; you just have not found a system that works for you yet.

Let me be real with you. The turning point for me was not an app or a sudden raise. It was white envelopes. Learning about cash stuffing, for beginners, changed my life. When you are living on the edge, using a credit card is dangerous because it does not feel real. Cash feels real. It makes you stop, look at what you have, and make a choice.

By the end of this post, you will know exactly which envelopes to start with, even if money is really tight right now.

What is Cash Stuffing?

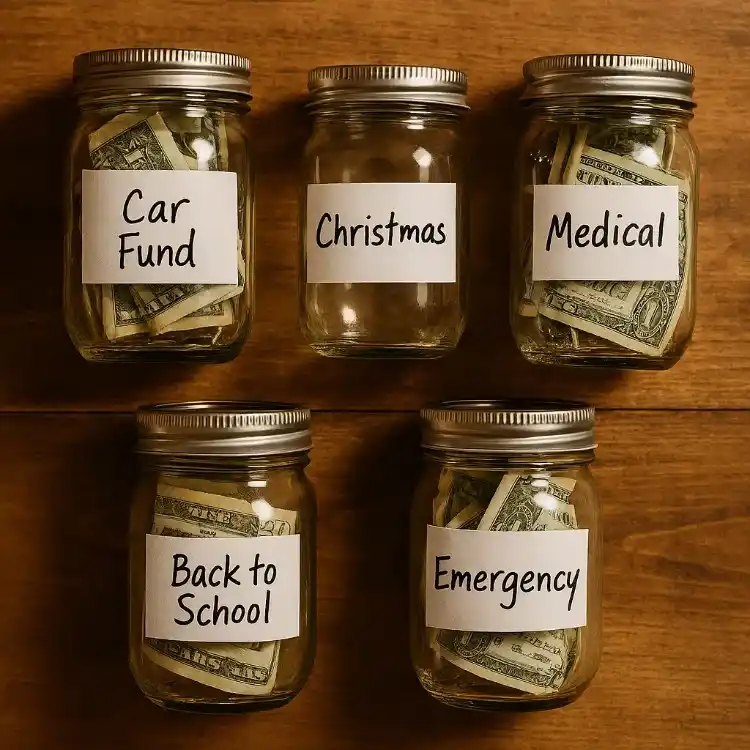

What is cash stuffing? Cash stuffing is a physical budgeting method where you take your paycheck in cash and divide it into labeled envelopes for different spending categories. When an envelope is empty, you stop spending in that category until your next payday.

It is really that simple. You might have heard your grandparents talk about the envelope system. Or maybe you’ve seen the modern version online, where people use a fancy cash stuffing binder. It’s the same concept. Dave Ramsey popularized the envelope budgeting method years ago, but it has made a massive comeback lately. Why? Because it works.

Even experts at NerdWallet explain the psychology of cash — it literally hurts your brain to hand over physical money. When you swipe a debit card, it feels like nothing. When you hand over a $20 bill, you feel the loss. And that is exactly what stops the overspending. You’ve got this.

Why Cash Stuffing Works for Low Income

When you are living paycheck to paycheck, budgeting advice can feel insulting. People tell you to “invest 20%” when you can barely afford eggs. I get it. Here’s the thing… cash stuffing is different. It is built for survival mode.

You see exactly where every dollar goes

There is no guessing. You look inside the envelope. If there is a $10 bill left, you have $10. The math is already done for you.

No app or internet needed — just cash

You don’t need a fancy smartphone app that syncs to your bank. You just need the money in your hands. It is entirely foolproof.

Stops overspending before it happens

You physically cannot overdraw your bank account if you leave your debit card at home. Overdraft fees become a thing of the past.

Builds a money habit, not just a plan

Budgeting on paper is a plan. Stuffing cash into envelopes is a physical habit. Habits change your life.

When I started, I had maybe $600 to work with each month after my rent was paid. I thought budgeting was for people with extra money. I was wrong. Budgeting is how you get out of the hole.

What You Need to Start

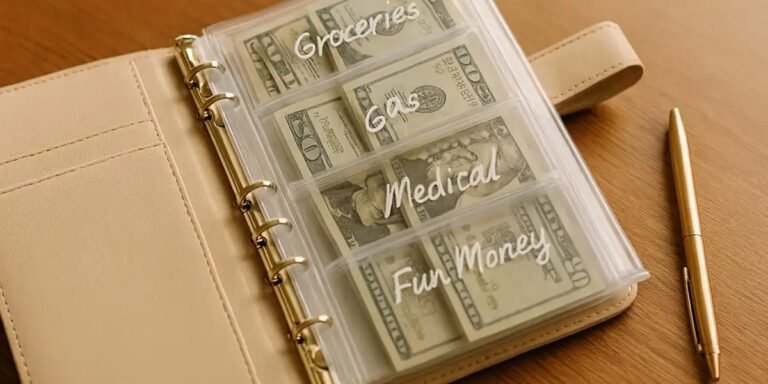

You do not need to spend money to start saving money. Do not go buy an expensive cash stuffing binder today. Just don’t. Keep it incredibly cheap and simple.

Here is what you actually need:

- A box of plain white envelopes ($1 from the dollar store)

- A pen or marker

- Your upcoming paycheck information

- 30 minutes of quiet time

Before you write on a single envelope, you need a plan. Stop reading for a moment and create your bare bones budget right now. You have to know exactly what you must pay just to survive the month. A cash stuffing binder is a fun optional upgrade for later, but today, we stick to the basics.

You do not need to spend money to start saving money.

How to Start Cash Stuffing: Step by Step

I know this sounds too simple, but the best systems always are. Here is the exact playbook to get started this week without overwhelming yourself.

1. Know your exact take-home income

Look at your paystub. Do not guess. You need the exact dollar amount that hits your bank account after taxes.

2. Write down every single expense

List out your rent, your electric bill, your groceries, and your gas. Every single thing that costs money this month goes on paper.

3. Choose your envelope categories

Pick the categories you usually overspend on. Label your envelopes with your marker. We will go over the exact categories in the next section.

4. Go to the bank and withdraw cash

Drive to the bank or ATM. Pull out the exact amount of cash you need for your variable expenses.

The first time I walked out of the bank with cash divided into categories felt oddly powerful. I was holding my month’s survival in my hands, and I finally felt in control.

5. Stuff your envelopes on payday

Sit at your kitchen table. Put $150 into the Grocery envelope. Put $40 into Gas. Do this until the cash is gone.

6. Spend ONLY from the envelopes

When you go to the store, take the Grocery envelope. Leave your debit card in a drawer at home. No, seriously. Leave it.

7. Review at the end of the month — adjust

Did you run out of grocery money in two weeks? Did you have $10 left in gas? Adjust your numbers for next month.

Advice: Keep your bill money (rent, car payment) in your checking account and pay them online. Only cash for your daily spending!

Best Cash Stuffing Categories for Low Income

If you look online, you will see people with 40 different envelopes for things like “Nail Salon” and “Vacation.” Ignore them. When you are broke, you need to master the basics.

GROUP A: MUST-HAVE ENVELOPES (do these first)

These are your survival cash envelope categories. If you only make 5 envelopes, make these.

1. Rent or Mortgage

Keeping a roof over your head is priority number one. Period.

If your rent is $700, this envelope gets $700. Non-negotiable.

Advice: If you pay rent online, leave this money in the bank. You don’t need a physical envelope for it.

2. Groceries

This is where almost everyone blows their budget. Food is expensive, but it is also the easiest place to cut back.

$150 to $250 for 1-2 people. Meal plan before you shop.

Advice: To make this envelope stretch, use my Aldi meal plan for a $50 week strategy. Take exactly $50 cash into the store. When it’s gone, you leave.

3. Utilities (electric, water, gas)

The lights must stay on.

Estimate based on last month’s bill. Add a small buffer.

Advice: Call your electric company and ask for “budget billing” so your payments are the same all year round.

4. Transportation or Gas

You have to get to work to make the money.

$60 to $120, depending on your commute.

Advice: Fill up your tank on payday using this cash. Only drive to work and the grocery store until you build up some savings.

5. Phone Bill

A phone is a necessity for work and emergencies.

Fixed cost — stuff it on day 1.

Advice: If your bill is over $40, switch to a cheap prepaid carrier immediately.

GROUP B: IMPORTANT ENVELOPES (add these next)

Once your basic survival is covered, add these to start getting ahead.

6. Debt Payoff

The minimum payments are eating your income alive. We have to attack the debt. Read my guide on how to get out of debt with no money to start.

Even $25/month toward debt matters. Seriously.

7. Emergency Fund

A flat tire shouldn’t ruin your life. A $50 unexpected bill shouldn’t mean you go hungry.

Start with $20. I mean it. $20.

Small is nothing. Small is a start.

8. Medical or Health

You will get sick. You will need ibuprofen or a co-pay for the clinic.

Co-pays, prescriptions, unexpected needs — $30 to $50 buffer.

9. Household Supplies

You need toilet paper, laundry detergent, and dish soap.

Cleaning products, toiletries, paper towels — $20 to $40.

GROUP C: OPTIONAL BUT POWERFUL ENVELOPES

(Add these when you are ready)

10. Personal Care

A cheap haircut or a bottle of lotion so you feel human.

11. Kids or School

Field trip money, a new pack of markers, or a school t-shirt.

12. Fun Money

Even $10 for yourself matters. Burnout kills budgets.

13. Clothing

Socks wear out. Kids grow fast. Put $5 a month in here.

14. Gifts or Holidays

Birthdays happen every year. Save a little each month.

15. Car Repair Sinking Fund

Oil changes and brake pads are inevitable. Save a little now.

Start with Group A only. Master those 5. Then add more.

Bare Bones Version: What if You Only Have $800/Month?

I hear this all the time. “I don’t make enough to budget.” Let me be real with you. The less money you make, the more you desperately need to cash stuff.

When my income dropped to almost nothing, I had to get ruthless. I remember a month where my grocery budget was so small that I was eating plain rice and beans for six days straight. It was miserable. But it kept me out of payday loan debt.

If you are on an extremely low income, your 50/30/20 rule for low income goes out the window. Here is a realistic $800 a month survival breakdown:

| Envelope | Amount |

| Rent (Room share) | $400 |

| Groceries | $150 |

| Utilities | $80 |

| Gas/Bus Pass | $70 |

| Phone Bill | $30 |

| Household/Toiletries | $20 |

| Emergency Fund | $20 |

| Debt Minimums | $30 |

This is survival mode budgeting. And survival mode is okay. It won’t be like this forever. You need to survive today so you can build for tomorrow. Trust me on this one.

Cash Stuffing Mistakes Beginners Make

It is not perfect. Nothing is. You will mess up, and that’s okay. Here are the traps to avoid when figuring out how to start cash stuffing.

1: Making 20 envelopes on day one

You will get overwhelmed. Keep it to 5 envelopes max for your first month. Keep it simple.

2: Not withdrawing cash on payday

If you leave the money in your checking account, you will swipe your debit card. Go to the bank on Friday morning. Make it a routine.

3: Robbing one envelope to feed another

Spending $20 from your grocery money on a pair of shoes defeats the entire purpose. When the envelope is empty, you stop. Period.

4: Quitting after one bad week

Budgeting takes 90 days to feel normal. Month one is a disaster. Month two is messy. Month three starts to click. Don’t quit in month one.

5: Waiting until the “perfect time” to start

There is no perfect time. The toxic money habits that keep you poor won’t break themselves. Start this Friday with whatever money you have.

One bad week does not mean you failed. It means you are human.

5 Suggestions to Make Cash Stuffing Work on a Low Income

Ready to actually do this? Here are my best tips for the trenches.

- Stuff envelopes the SAME DAY you get paid: Do not wait until Monday. Money has a funny way of disappearing over the weekend.

- Use a pencil on envelopes — budgets change: Your gas budget might need to go up next month. Erase and rewrite.

- Keep a running total on the outside of the envelope: Write down what you spend like a mini-ledger. It keeps you honest.

- Do a 5-minute Sunday check-in each week: Look at your envelopes on Sunday night. Know exactly what you have left for the week ahead.

- Celebrate small wins out loud: Did you save $10 this week? Tell someone. Be proud of yourself.

The system is not the hard part. Starting is.

Ready to Take Control of Your Money? (Conclusion)

I know how tired you are. I know the stress of wondering how you are going to make it to next Friday. But you can take control back.

You don’t need a high-paying job to start. You don’t need a fancy aesthetic binder. You just need a few plain envelopes and the willingness to try something different. If money has been hard, that is not a character flaw. It is a circumstance. And circumstances change.

Learning cash stuffing for beginners was the single best thing I ever did for my peace of mind. It gave me my life back. It can do the same for you.

Now I want to hear from you. Which envelope category are you starting with first? Drop it in the comments below.

Frequently Asked Questions (FAQs)

Yes, absolutely. Cash stuffing is actually more effective for low-income earners because it forces strict discipline. When every single dollar matters, physical cash prevents accidental overdrafts and stops impulse buying dead in its tracks. It is the ultimate survival tool for a tight budget.

A beginner should start with 4 to 5 envelopes maximum. Focusing on your core variable expenses like groceries, gas, household supplies, and a small emergency buffer is plenty. Starting with too many categories causes overwhelm and makes you want to quit the system entirely.

Yes, you can still cash stuff your variable spending. Leave enough money in your checking account to cover your fixed online bills like rent, car payments, and utilities. You only need to withdraw cash for categories where you physically go to a store, like the supermarket or the gas station.

Yes, cash stuffing is the same as the envelope budgeting method. It is simply a modernized, popular term popularized on social media platforms like TikTok and Pinterest. The core concept of dividing physical cash into categorized envelopes remains identical.

You will see a difference in your bank account balance within the very first month. However, it typically takes about 90 days for the physical habit of using cash to feel completely natural. Give yourself three months of grace before deciding if the system works for you.